Journalism of Courage

Premium

This is an archive article published on October 1, 2012

Tata Power stock: Not all gloom

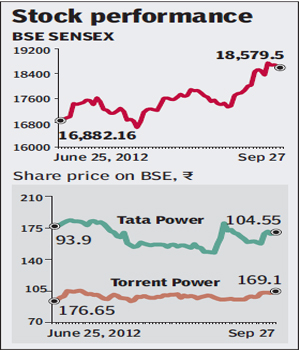

The Tata Power stock has underperformed the Sensex by 11% during last 12 months after commissioning of Unit 1 at Mundra which is running at an operating loss and also due to fall in international coal price impacting the companys profitability.

October 1, 2012 09:16 PM IST 4 min read

4 min read

Tariff relief at Mundra likely,stock offers upside despite lower coal prices

The Tata Power stock has underperformed the Sensex by 11% during last 12 months after commissioning of Unit 1 at Mundra which is running at an operating loss and also due to fall in international coal price impacting the company’s profitability. We expect marginal tariff relief at Mundra as highly probable and believe the stock offers upside despite lower coal prices. Upgrade to OW (V) from Neutral (V),raise net profit estimates by 11% for FY14 & TP (target price) to R125 (from R108) on 25 paise higher tariff recovery expectation at Mundra.

We believe tariff relief at Mundra is highly probable: We believe if central regulator (CERC) agrees that the case falls under its jurisdiction,it is likely to examine if Mundra project,where the tariff was determined through a bidding process,deserves a tariff relief as the project is operating at a negative return.

We believe tariff relief at Mundra is highly probable: We believe if central regulator (CERC) agrees that the case falls under its jurisdiction,it is likely to examine if Mundra project,where the tariff was determined through a bidding process,deserves a tariff relief as the project is operating at a negative return.

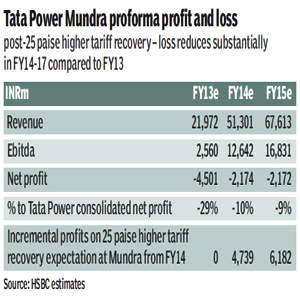

While the question itself is complex and far reaching for the private power companies,we believe that there is a general consensus among stakeholders that while generators should not be loaded with long-term fuel risk,they should also not be allowed to earn super-normal profit by controlling the fuel source. Hence regulator is likely to take a holistic view and also consider the earnings from their coal business while calculating the losses. We expect that the company is likely to get a relief of 25 paise of the 35-40 paise per unit loss expected in the initial 4-5 years. We also believe that litigation will be time consuming.

While the question itself is complex and far reaching for the private power companies,we believe that there is a general consensus among stakeholders that while generators should not be loaded with long-term fuel risk,they should also not be allowed to earn super-normal profit by controlling the fuel source. Hence regulator is likely to take a holistic view and also consider the earnings from their coal business while calculating the losses. We expect that the company is likely to get a relief of 25 paise of the 35-40 paise per unit loss expected in the initial 4-5 years. We also believe that litigation will be time consuming.

Our estimate results in additional net profit of R6.2 bn per annum for Tata Power (27% of FY15e net profit) raising our target price by R16/share. Despite assuming this tariff relief,the power tariff from Mundra project will be significantly lower (at R2.68 per unit for FY14) than any other imported coal-based project. For instance,the most recent imported coal-based project which is on a cost plus basis is getting a tariff of R4.2/unit (Lanco Udupi power project).

Our estimate results in additional net profit of R6.2 bn per annum for Tata Power (27% of FY15e net profit) raising our target price by R16/share. Despite assuming this tariff relief,the power tariff from Mundra project will be significantly lower (at R2.68 per unit for FY14) than any other imported coal-based project. For instance,the most recent imported coal-based project which is on a cost plus basis is getting a tariff of R4.2/unit (Lanco Udupi power project).

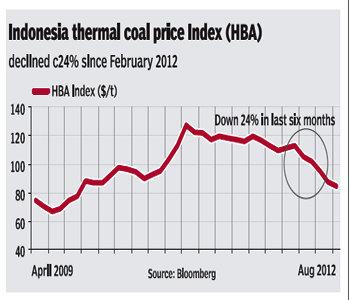

Decline in global coal prices has reduced profitability but we see prices remaining flat & limited downside: The profitability at its coal business (57% of FY12 Ebit) is expected to be under pressure in FY13 due to decline in coal prices. While Q1 prices have been at $84 per mt we expect the prices to remain at these levels over next few years. Even if prices declines further by $5/mt,downside risk is limited (0.9% on FY14 EPS). Separately,the risk of rupee strengthening by 10% can impact FY14 EPS by 1.7% negatively. Thus together in case of both these events happening,the downside is limited to c6% to our target price.

While on the upside,if the company is able to increase production faster than what we anticipate (100mt per annum by FY15),then the favourable impact on FY14 EPS (earnings per share) is about 3.7% and target price about 1%.

Story continues below this ad

Upgrade to OW: Our revenue and net profit estimates for FY13 declines largely due to our lower expectation of coal price realisation in its coal business to $84/ton (from $95/ton earlier). We raise our FY14 net profit estimates by 11% on 25 paise higher tariff recovery expectation at Mundra and target price to R125 (from R108),implying a potential return of 21.5% from the current share price. Our target price implies a 1.8x FY14e PB (price-to-book ratio) and 13.9x(times) FY14e PE (price-earnings ratio) compared to the current FY13e PB of 1.7x and PE of 15.8x.

We introduce our FY15 estimates and expect Tata Power to report an EPS CAGR (compound annual growth rate) of 9% over FY13-15e.Our net profit estimates for FY13-14 are largely in line with consensus if we exclude our expectation of tariff relief of 25 paise per unit on Mundra project. Assuming tariff relief our FY14 net profit estimate is higher by 33% to consensus.

We upgrade the stock to Overweight (V—with volatility) from Neutral (V) and expect announcement of any tariff relief to act as catalyst for stock price movement. This is also a key risk to our call. If this does not go through,the upside on the stock remains moderate at 5%.

HSBC

Advertisement

Live Blog

Advertisement

PHOTOS

Top Stories

Advertisement

Must Read

SportsTemba Bavuma: South Africa's Iron Man with a giant heart, undefeated and unbroken, leads from the front at Eden Gardens for famous win

SportsPramod Bhagat and the art of not giving up: How former Paralympics champion shuttler bounced back from anti-doping ban

Advertisement

Buzzing Now

TrendingAkon ‘harassed’ on stage in Bengaluru, viral video shows fans pulling singer’s pants during concert: ‘India has no respect for any artist’

TrendingMaharashtra man makes donkeys pull SUV in protest against dealership over ‘faulty car’; video goes viral

TrendingBihar man gets abused, slapped by Patna police in viral video, later gets threat calls: 'Delete it quickly or we will arrest you'

- 01

- 02

Advertisement