© IE Online Media Services Pvt Ltd

Journalism of Courage

Coal India might seem like just another government-run miner, but here’s the twist: it offers a 7.2% dividend yield. (Express archive/ Partha Paul)

Coal India might seem like just another government-run miner, but here’s the twist: it offers a 7.2% dividend yield. (Express archive/ Partha Paul)The world loves a good story. And for the last few years, that story has been about renewable energy, about a clean and green future. But here’s the thing — India still runs on coal. 72% of its electricity comes from coal-fired power plants.

The world loves a good story. Lately, that story has been about renewable energy and a cleaner, greener future. But here’s the reality: India still runs on coal, with 72% of its electricity coming from coal-fired power plants.

Coal India, which commands an 80% share of the country’s coal production, saw a strong rally from 2020 to 2024. But that momentum has faded — the stock has been in a downtrend for the last seven months, pulling back from its peak of ₹530 per share.

Source: http://www.tradingview.com

Source: http://www.tradingview.com

Why the slide? And could this dip be an entry point for long-term investors?

Coal India might seem like just another government-run miner, but here’s the twist: it offers a 7.2% dividend yield. What’s more interesting is that PPFAS, a mutual fund known for sticking to its value-investing principles, has been steadily increasing its stake since 2022.

So why would PPFAS buy into an industry that’s supposedly dying? We believe the inconvenient truth is: Coal isn’t going anywhere

Coal-based power accounts for 47% (218 GW) of India’s total installed capacity, a number that looks promising for green energy — because it means non-fossil fuel sources make up the rest. But installed capacity and actual power generation are very different.

Solar and wind have grown, but their plant load factors (PLF) — a measure of how much of their capacity they actually use — remain low: 15.7% for solar and 21% for wind. In contrast, coal-powered plants operate at a robust 68.48% PLF.

Fig 2: Source: https://iced.niti.gov.in/energy/electricity/generation

Fig 2: Source: https://iced.niti.gov.in/energy/electricity/generation

This means that coal plants generate 72% of the total electricity in India, even though their installed capacity is below 50%.

And it gets even more interesting.

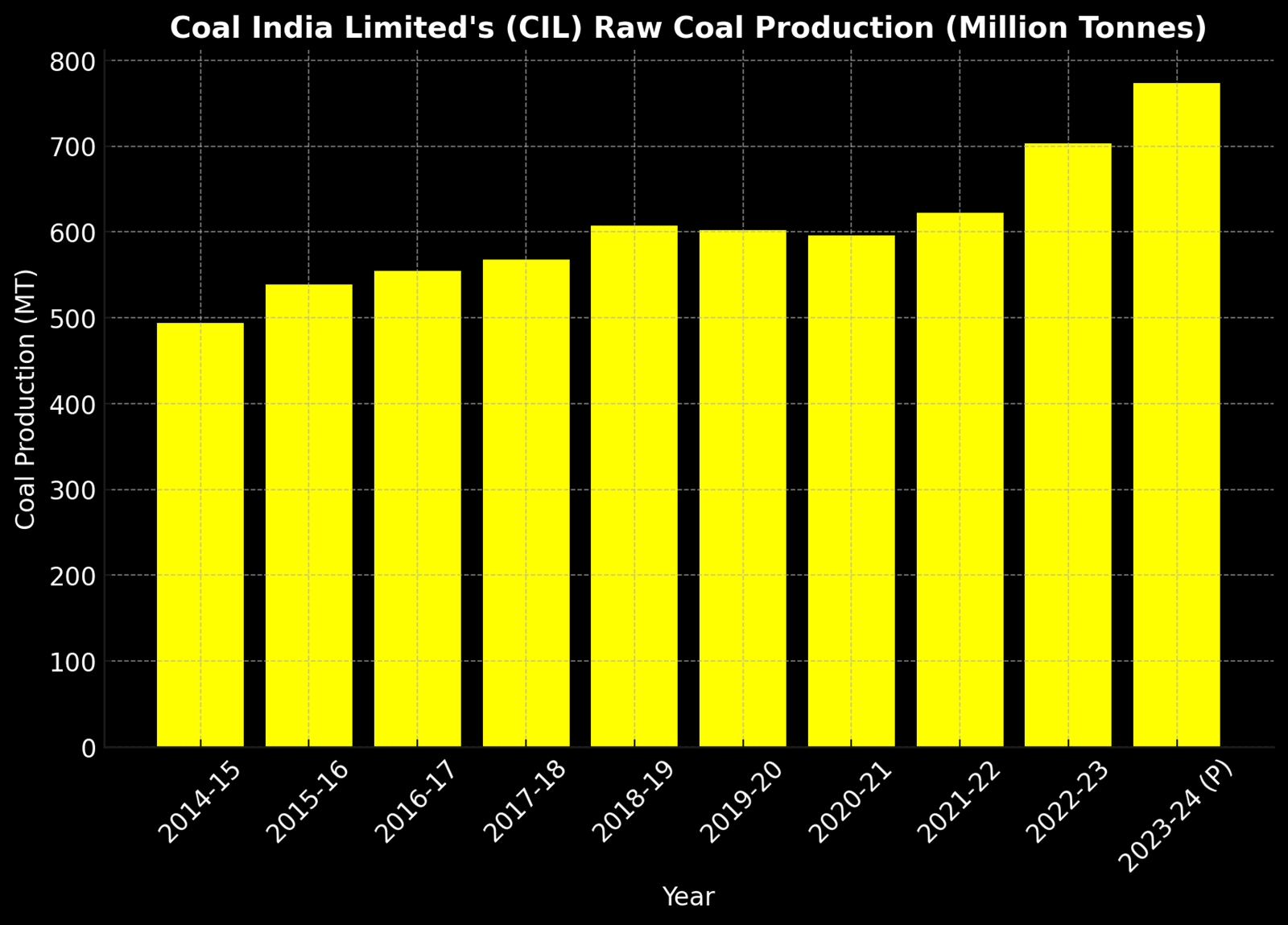

Coal consumption in India has been rising for the last five years. Coal India plans to increase production to 1 billion tonnes by FY26.

Even then, it won’t be enough.

Coal India Limited’s raw coal production. (Source: Coal India Annual Reports / Company presentations)

Coal India Limited’s raw coal production. (Source: Coal India Annual Reports / Company presentations)

In FY24, India used 1,264 million tonnes of coal. But it only mined 964 million tonnes domestically, importing the remaining 300 million tonnes.

Coal type-wise import trend. (Source: https://iced.niti.gov.in/energy/fuel-sources/coal/import)

Coal type-wise import trend. (Source: https://iced.niti.gov.in/energy/fuel-sources/coal/import)

The bulk of these imports? Non-coking coal for power plants.

This is why both Coal India and the Indian government are pushing for higher domestic production. This will help in 1) reducing reliance on expensive imported coal, and 2) supporting 52.7 GW of new thermal power (coal) plants in the pipeline.

Despite the belief that coal is on its way out, the government is already commissioning new coal plants. 12.8 GW of greenfield coal capacity was awarded within the first 100 days of the new administration.

So coal is here to stay. And so is Coal India, which still accounts for 78% of the country’s coal production.

Coal India operates through eight subsidiaries, mining about 80% of the country’s coal, most of which goes to state utilities for power.

Fig 5: Source: CIL Q3FY25 Presentation

Fig 5: Source: CIL Q3FY25 Presentation

The company’s top line depends largely on three levers:

Take 2022, for example. Coal shortages after the COVID reopening led to higher pricing per tonne, boosting profitability.

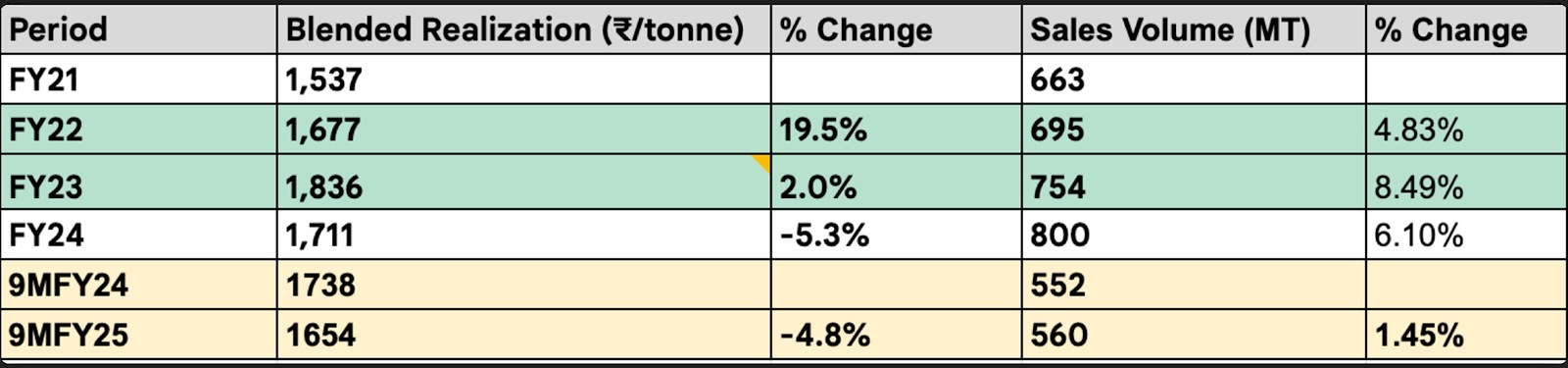

Source: Axis Securities Results Update / 28th January 2025

Source: Axis Securities Results Update / 28th January 2025

But in FY24, volume growth slowed, and pricing remained subdued. As the table below shows, 9MFY25 volumes grew just 1.5%, while blended realizations dropped by about 5%.

Source: CIL company presentations, filings, Annual Reports

Source: CIL company presentations, filings, Annual Reports

This subdued volume growth might be a seasonal phenomenon and is likely to recover. The last quarter always accounts for the highest coal production and dispatch.

Source: http://www.tijori.com

Source: http://www.tijori.com

Still the big question remains — was FY22-FY24 an exception? Or is there something deeper happening? Can volume growth truly hit double digits in the coming years?

For years, Coal India operated in a predictably inefficient way where volume growth was hard to come by. But since 2021, something has shifted. Not only on the volume growth front but also on costs.

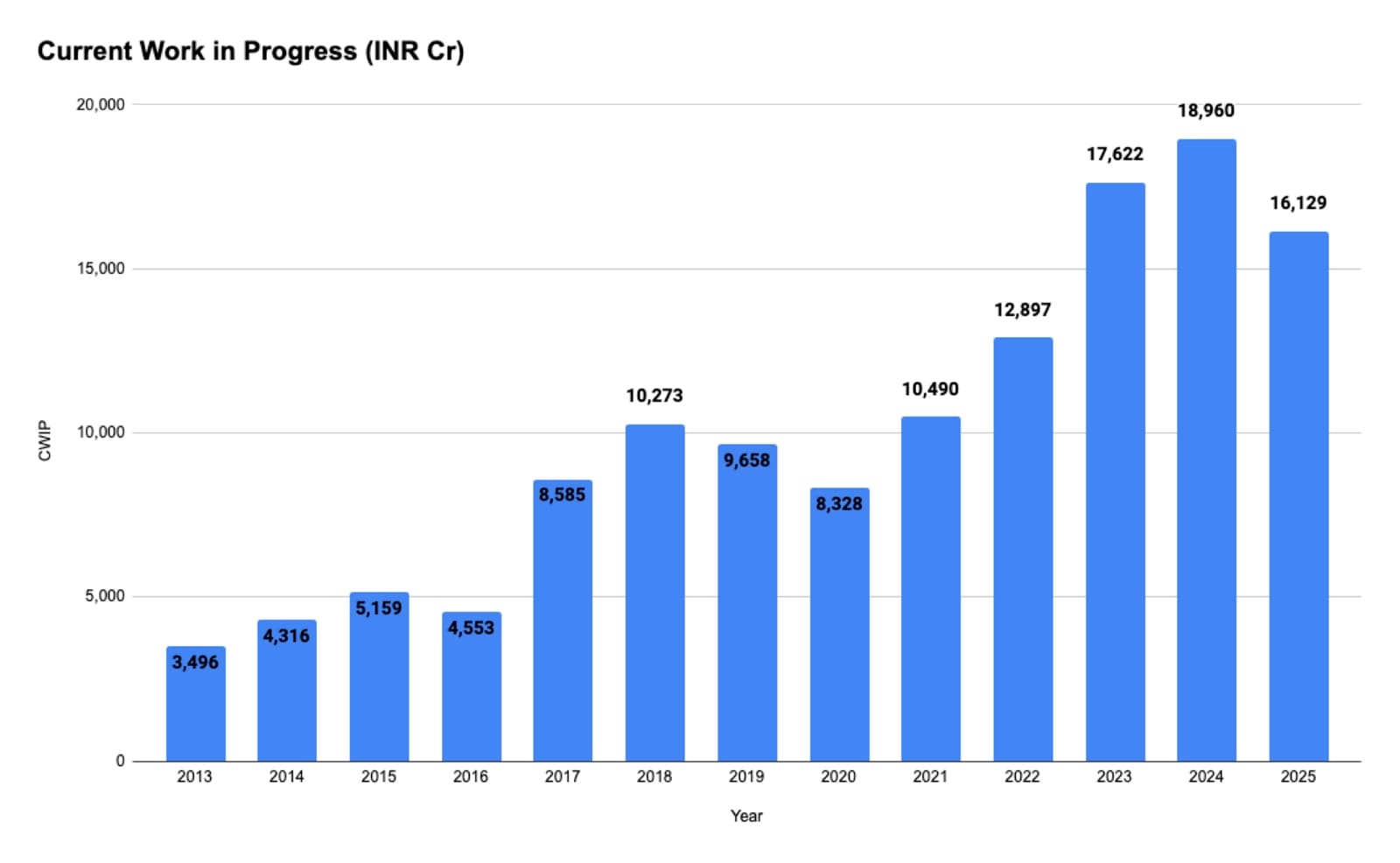

Look at CWIP (Capital Work in Progress) on the balance sheet. The company has been investing heavily in expanding capacity.

Source: http://www.screener.in

Source: http://www.screener.in

Here’s what those investments are:

₹15,500-16,500 crore annual capex for FY25-FY27 — focused on coal washing, mining expansion, first-mile connectivity (FMC) projects, and rail infrastructure.

Approval granted to 119 new coal projects, with a combined production capacity of 896 MTPA.

15 Mine Developer & Operator (MDO) projects are set to contribute 173 MTPA, with six already operational. While production in FY24 stood at 9.55 MTPA, it is showing signs of improvement.

First Mile Connectivity (FMC) initiatives are being implemented to enhance coal transportation efficiency and ease congestion. The company is building rail infrastructure in Odisha, Jharkhand, and Chhattisgarh to speed up coal movement. By FY29, three phases of FMC projects will add 914.5 MTPA of rapid loading capacity. This matters because bottlenecks in transportation lead to coal shortages, inefficiencies, and increased costs. Solving that problem could be a game changer.

Critical Mineral value chain: CIL is strategically investing in new business segments which includes lithium, nickel, cobalt, and graphite sectors.

Green energy: CIL has an ambitious plan of installing 3 GW of renewable energy by 2025-26 and 5 GW by 2029-30

CIL is also making radical changes to its cost structure.

Manpower costs account for 48% of total expenses and has been a source of contention. This is changing as the company plans to reduce manpower annually by 5% for the next 5 years. And this isn’t just a “plan”, it’s already happening. There was a net reduction in manpower by 10,349 employees during FY 2023-24, leading to a net reduction of 1% in manpower costs.

And because coal mining is a high operating leverage business, a small increase in volume growth or a small decrease in costs leads to a multiplier effect on the bottom-line.

If it all works, Coal India will become more efficient, more profitable, and also reduce the country’s coal import bill in the process.

But what if it doesn’t?

Even if none of this plays out as expected, Coal India still has one major advantage: its dividend yield.

At 7.2%, it’s basically a fixed deposit, except with the potential upside of a stock if volume growth improves.

There’s no guarantee the stock won’t drop further. But the downside risk seems limited, while the upside is a real possibility.

For a patient investor such as PPFAS, this might not be such a bad idea.

Note: We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Rahul Rao has helped conduct financial literacy programmes for over 1,50,000 investors. He also worked at an AIF, focusing on small and mid-cap opportunities.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.