© IE Online Media Services Pvt Ltd

Tags:

HDFC Bank had been trading in a narrow range between Rs 1,300 and Rs 1,700 per share for 40 months until mid-September 2024, when it “broke out” of this range, signaling a potential turnaround.

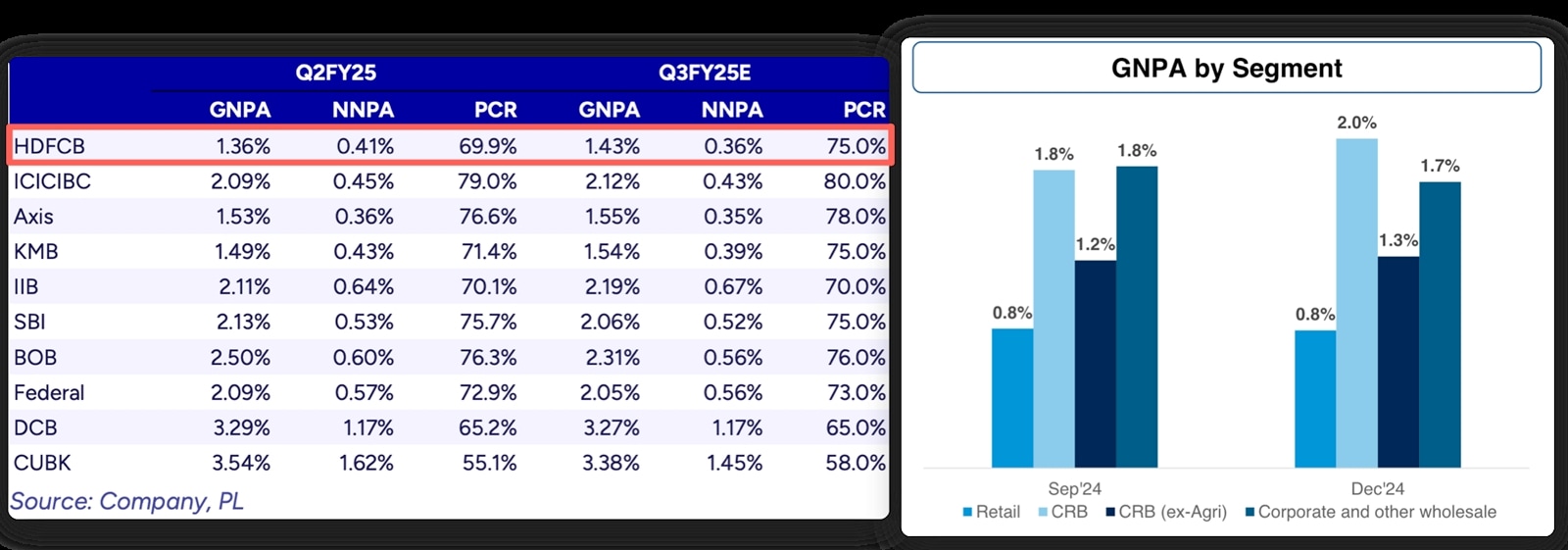

Unlike many banks that struggle with credit growth because of their poor asset quality, HDFC Bank’s credit USP remains intact. Despite a marginal increase in Gross Non-Performing Assets (GNPA) between Q2FY25 and Q3FY25, its credit growth at 1.43% is the lowest among peers.

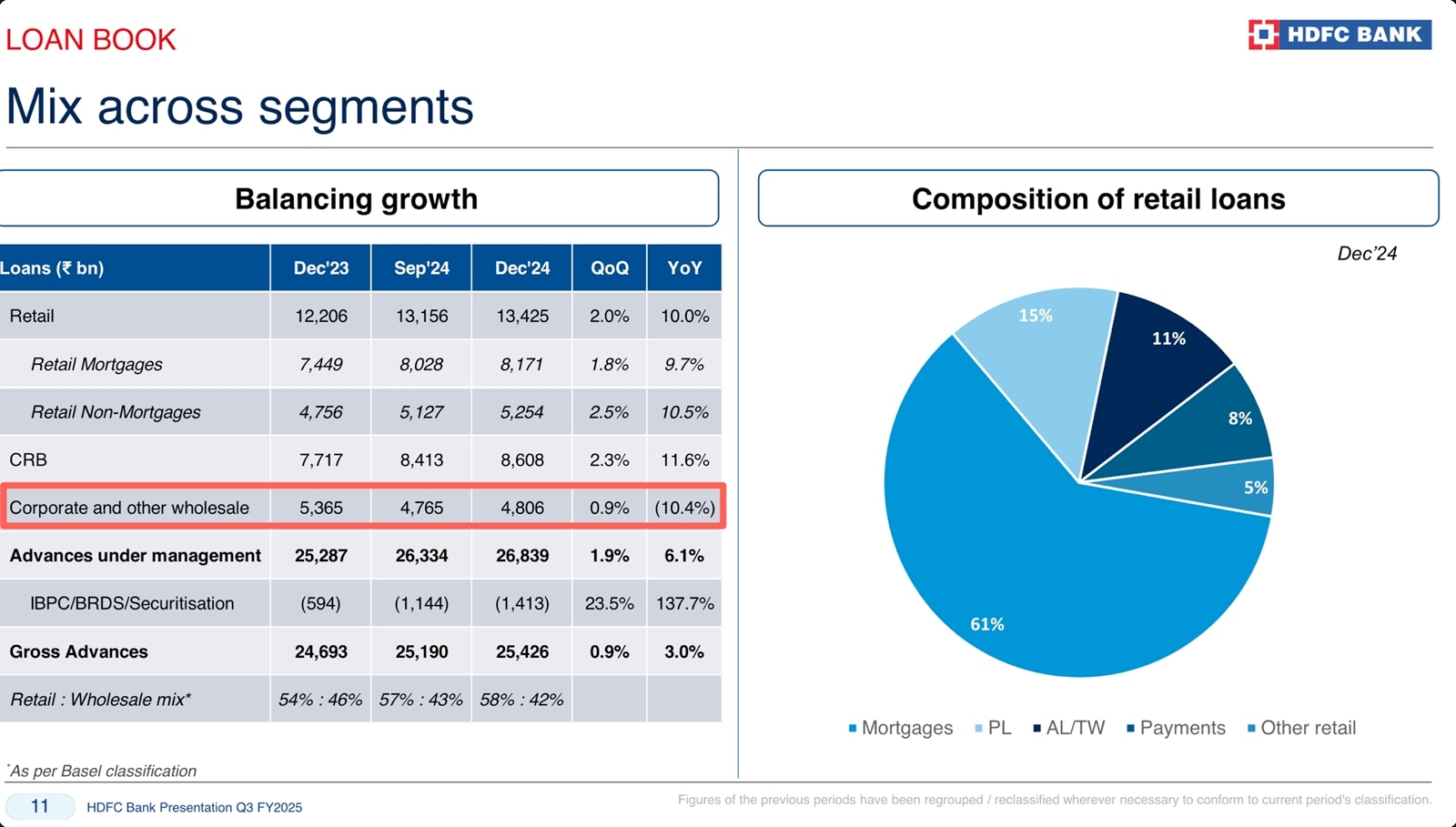

For its retail book, which constitutes nearly 58% of the total loan book, its GNPA is even lower at 0.8%.

As evident from the charts above, the major increase in total value of NPAs is because of CRB (Commercial & Rural loan book), mainly on account of agri loans and corporate and other wholesale loans which the bank has reduced by 10% YoY.

HDFC Bank has been intentionally moderating its growth in FY25 to improve its Loan-to-Deposit Ratio (LDR). A high LDR poses liquidity risk, as excessive lending leaves fewer reserves for withdrawals. It also increases funding costs and forces reliance on external borrowing — factors that make the Reserve Bank of India nervous too. That’s why bringing down the LDR has been a key agenda for HDFC Bank.

It aims to bring LDR back to pre-merger levels, which was in the mid-80%. In Q3FY25, the bank’s LDR improved to 98.2%, compared to 99.8% in the previous quarter and 110% at the time of its merger with HDFC Limited in July 2023.

This cautious approach led to slower growth in some segments. While overall advances grew at 3% YoY, retail loans grew at 10.1%. Within retail, mortgages grew by 11.7% YoY, and non-mortgage retail grew by 10.7%. Meanwhile, corporate and other wholesale loans declined by 10.4%.

In its Q3FY25 earnings call, the bank’s management noted that large ticket-size corporate loans are sensitive to interest rates, and loan spreads in the market are under pressure. As a result, the bank chose to moderate growth in this segment rather than compromising on loan pricing.

On the deposit front, HDFC Bank recorded a growth of 16.9% in Q3FY2 compared to average system deposit growth of 11.8% in H1FY25 (based on data of 36 banks and small finance banks) and 13% of old private sector banks. This underscores the bank’s competitive ability.

HDFC Bank has been working to integrate its branch network post-merger.

Over 80% of the bank’s branches are now capable of servicing accounts from the merged entity. In addition, the bank has added over 1,000 branches in the last 12 months, growing their network at 13% YoY. With nearly 38% of the branches less than three years old, productivity gains are expected.

HDFC Bank also converted approximately 1.9 million customers of the 4 million HDFC Ltd accounts (prior to merger) into customers who have deposits with the bank now. These were primarily new-to-bank mortgage customers who are being converted to also hold liability accounts with the bank. The bank aims to further expand its wallet share among these converted customers by cross-selling other retail products. For example, 250,000 of these customers have been given other products such as credit cards.

The merger’s initial challenges — higher cost of borrowings, higher LDR ratio, higher cost to income — are now beginning to see green shoots of merger synergies.

The bank has indicated its growth strategy to its shareholders. It intends to grow slower than system credit growth in FY25. In FY26, it plans to match system credit growth and in FY27, it expects to exceed the overall credit growth.

This approach will allow the bank to re-orient itself in a challenging environment, improve its LDR, and resume its growth journey. It is well-capitalised to support this growth.

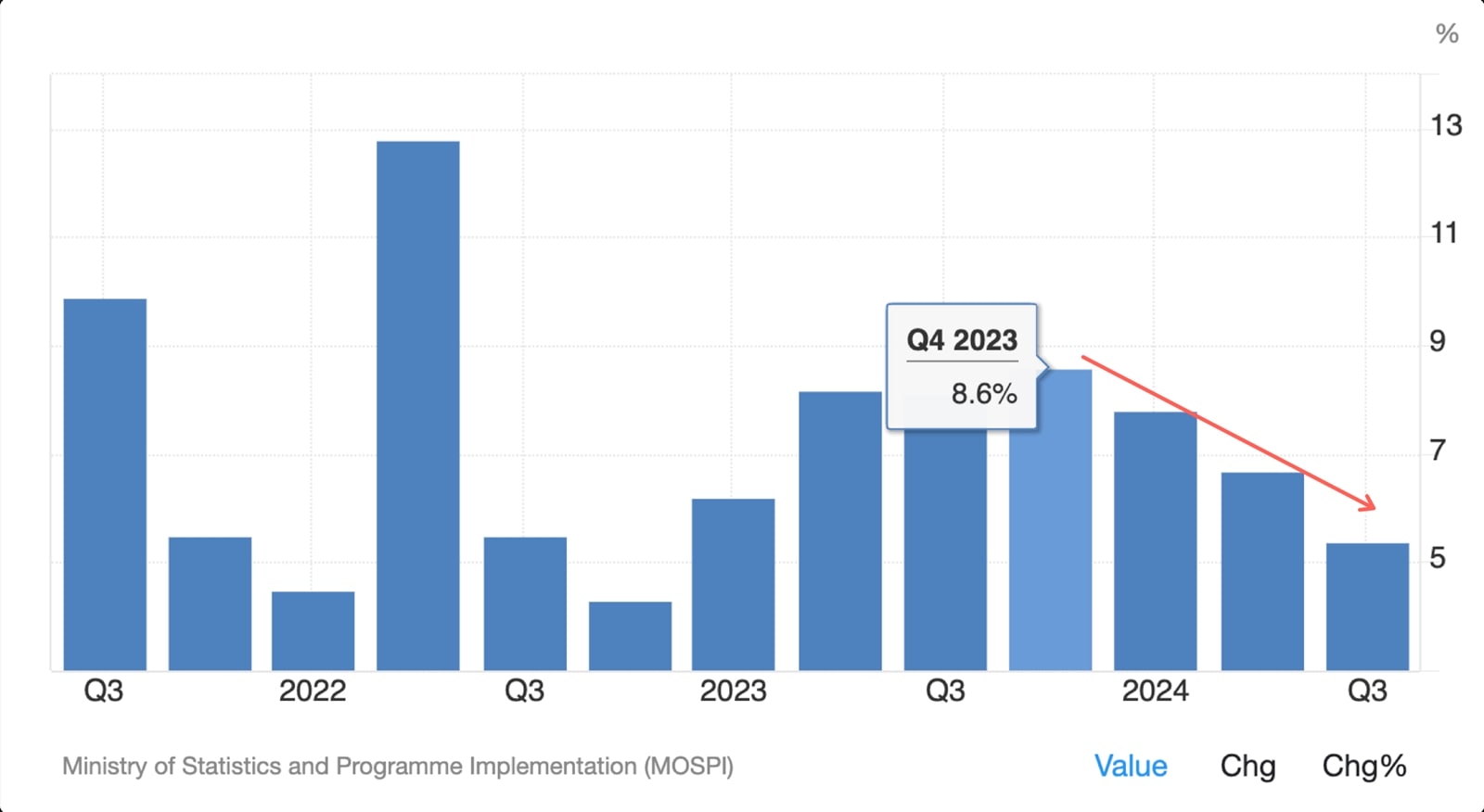

It is believed that credit growth and GDP growth has a direct and positive correlation. While GDP growth in certain sectors is more sensitive to credit growth, credit growth itself is vital.

Owing to liquidity shortages and higher rates, credit growth on India level has been contracting. From 20%+ in February 2024, it has come down to 11.5% in February 2025, accompanied by contracting GDP growth.

This needs to change.

Part of the decline is being attributed to low liquidity in the banking system. The RBI has recently announced a host of measures to infuse Rs 1.5 lakh crore into the banking system. Additionally, the central bank also announced a 25-basis point repo rate cut, signalling a move towards a more accommodative monetary policy.

This is likely to allow the banks to lend more at lower rates, which will lead to a resurgence in credit growth and GDP growth. In an environment that supports this growth, HDFC Bank is increasingly becoming adept at making the most of these opportunities.

Whether HDFC Bank’s quiet turnaround is for real, or just a flash in the pan, only time will tell. But given its long history of strong delivery, it may be best to watch these signals.

Note: We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Rahul Rao has conducted financial literacy programmes for over 1,50,000 investors and has worked at an AIF, focusing on small and mid-cap opportunities.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.